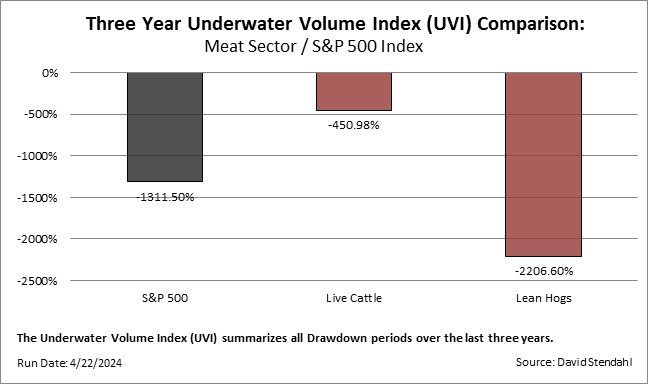

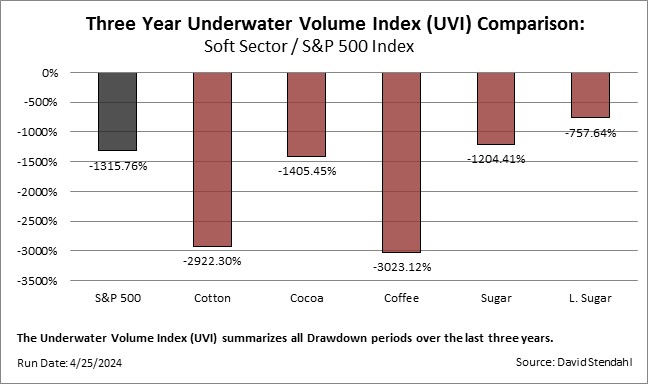

Risk Profile Comparison:

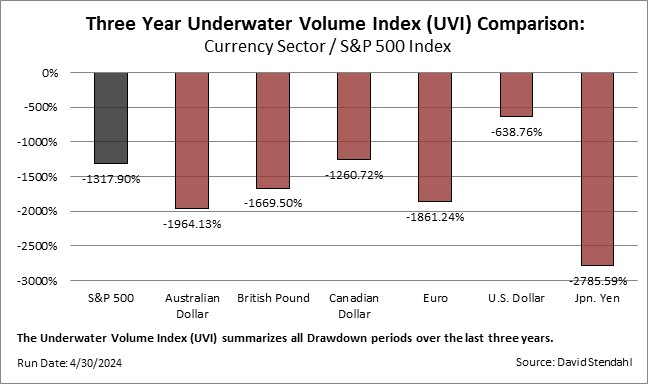

The Underwater Volume Index (UVI) is a measure of risk that sums up total drawdown over a set time period. Unlike maximum drawdown, which measures loss at a specific point in time, the Underwater Volume Index adds up all drawdown periods into a single number. This cumulative measure provides a clear perspective of true risk. As an example, Market A had a maximum drawdown of 15% but it was able to recover quickly as it went onto make consistent new market highs. Market B, on the other hand, languished in an extended drawdown period that lasted for years but only experienced an 8% max drawdown. Based solely on maximum drawdown it would be assumed that Market B experience less risk. Reviewing the UVI for the two markets could in fact, tell a very different story. The Underwater Volume Index for Market A could actually be less than Market B’s simply because of the prolonged drawdown period.

The study below compares the Underwater Volume Index for each Currency market alongside the S&P 500 Index. Markets with smaller UVI numbers will have experienced less drawdown exposure over the three year test period than those with higher UVI levels. A quick look at the UVI comparison chart below should provide some much needed clarity on true risk.

Definitions:

- Underwater Volume Index (UVI) summarizes all monthly drawdown periods.

- Maximum Drawdown measures the largest peak-to-valley loss based on monthly return data.

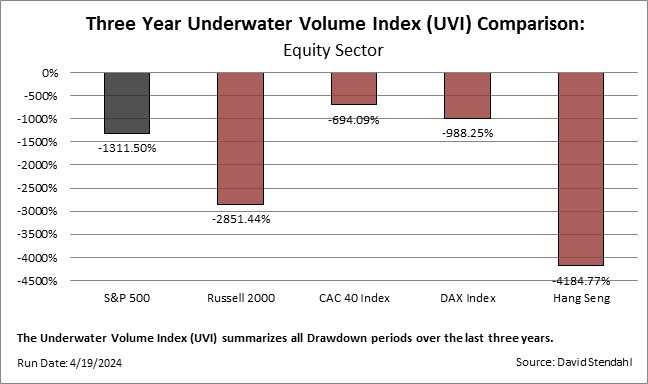

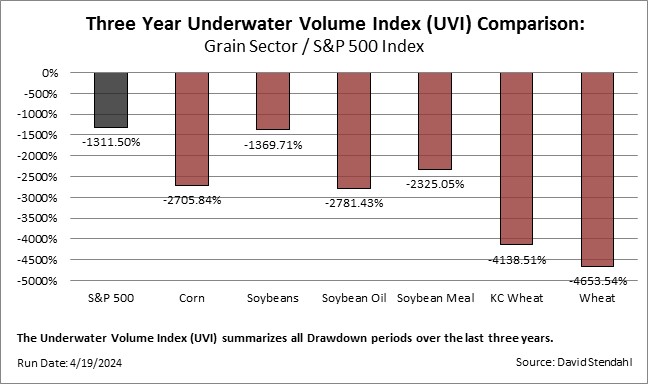

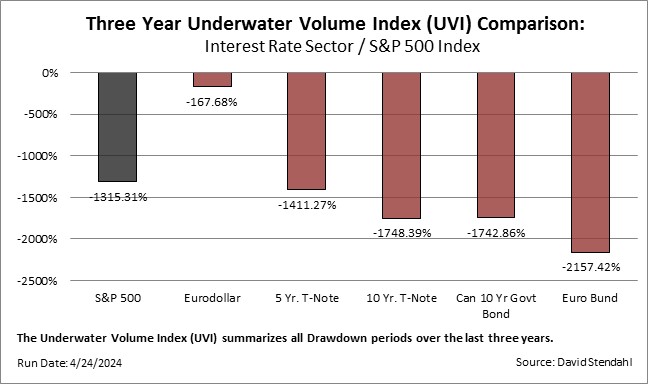

Sector Breakdown based on the Underwater Volume Index (UVI) :